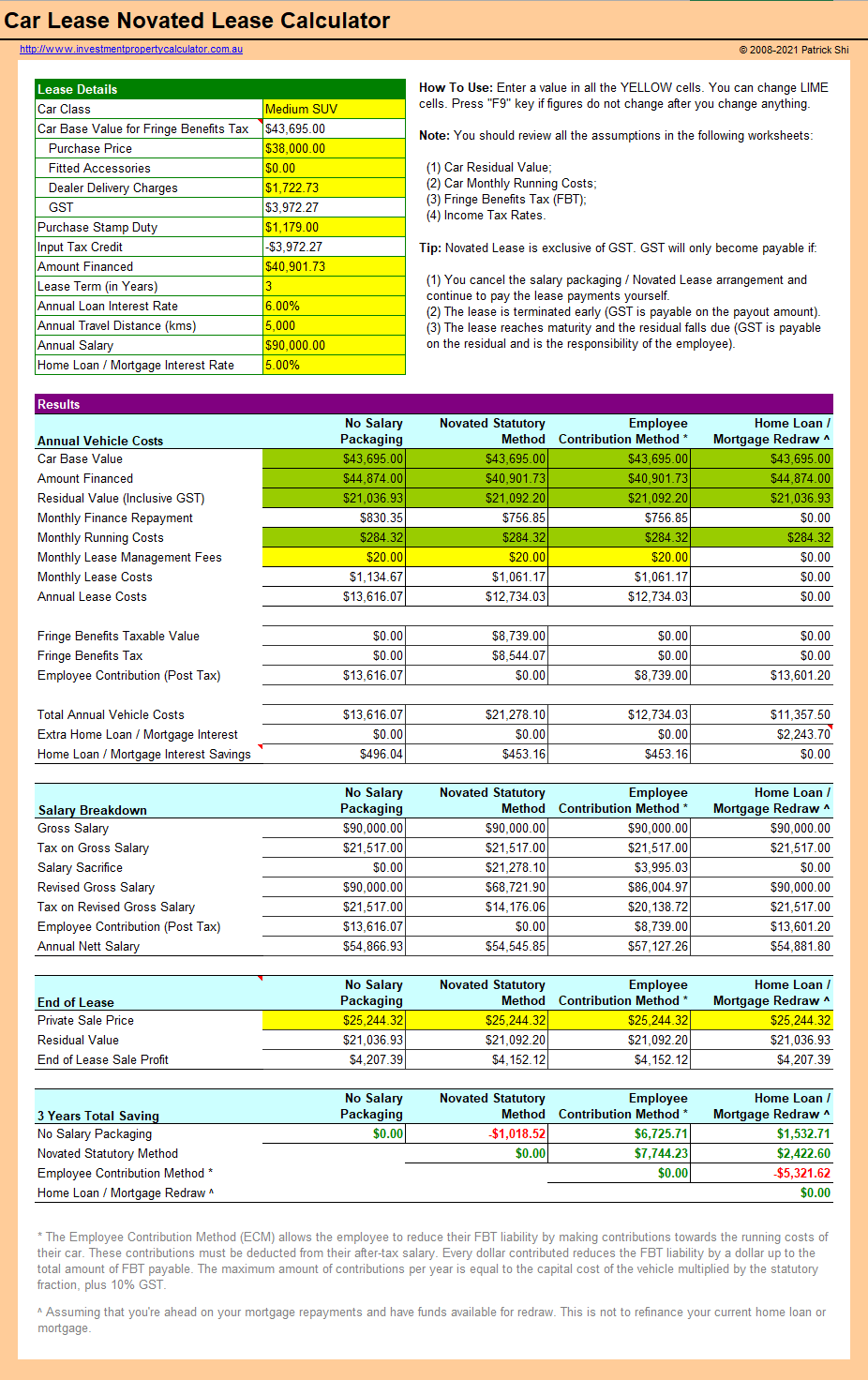

Calculator For Novated Lease

iqrasaad091@gmail.com

Leasing a car can be a great alternative to other financing options if youâr (48 อ่าน)

29 ก.ย. 2568 22:32

Leasing a car can be a great alternative to other financing options if youâre not quite ready to buy. It essentially allows you to borrow a vehicle for a short-fixed duration with lower monthly and down payment costs. To avoid spending more money in the long run, itâs important to do your research and pay attention to the fine print. To help you out, weâve compiled a guide outlining the disadvantages and benefits of leasing a car, as well as the best leasing options that will help you save money on your next vehicle Calculator For Novated Lease.

What is a car lease?

A car lease allows you to drive a brand new vehicle for a fixed period at an agreed monthly rate. Leasing doesnât require a car loan approval or a hefty payment up front, but unlike typical financing plans, monthly lease payments go toward the use of the vehicle instead of the ownership of the vehicle. In other words, itâs essentially a long-term rental, and once the fixed lease period is over (typically between 2 to 4 years), then the customer must either return the car to the leasing company or purchase it for market value.

Leasing a car requires a down payment and monthly payments consisting of rental charges, interest, taxes, and the depreciation costs of the vehicle over time. The interest rate and fees can vary based on the vehicle you are leasing.

Benefits of leasing a car

There are plenty of benefits to leasing a new car, the main one being lower payments. The reason leasing a vehicle is beneficial is that you only pay for the depreciation of the car. Leasing is also a great option if youâre someone who struggles with commitment issues and canât decide on a vehicle model? Or what interior to choose? A typical car lease contract only lasts 2 to 4 years and spans the early, problem-free days of a vehicle.

Once the contract is over, you can trade in your car for an upgraded model, a new colour, or a different vehicle entirely! This comes with the added perk of always being up to date on car manufacturersâ latest features and technologies while driving a brand new car more frequently, and this gives you a shot at a fresh manufacturer's warranty every few years, which may even include free maintenance such as oil changes and servicing.

So long as you can drive within the mileage cap outlined in your contract and avoid any major wear and tear damages to the car, you shouldnât incur any additional fees outside of your monthly payment, regardless of the vehicle you choose.

Disadvantages of leasing a car

Before getting too excited about the low-cost, low-commitment pros of leasing a car, itâs important to understand the cons as well. The obvious downside to leasing a car is the fact that, despite making monthly payments, you never actually own the car that youâre driving. Once the lease term ends, youâre required to return the vehicle and restart the process from scratch, with no equity to use toward the purchase of your next ride. This is the key difference between leasing and buying (or financing) a car.

While it may be tempting to jump on an apparently low price tag at first, be careful because, in the long run, it could actually cost you more. Itâs easy to get carried away in the cycle of upgrading your vehicle every 2 to 4 years, but repeatedly leasing cars over time will actually carve a deeper hole in your pocket than a one-time car purchase would, and in the end, youâll have no vehicle to truly call your own.

Another aspect to carefully consider is the vehicle lease contract. Every car lease contract is embedded with rather restrictive guidelines, and if you fail to follow them, you could face costly penalty fees. These guidelines may include a mileage cap, as mentioned above, which restricts you to an annual kilometre limit (typically around 25,000 km/ year) that youâre expected to stay below. If you have a long commute to work or plan on making a few road trips, then you could face steep charges at the end of your lease term. For many Canadian drivers living in rural communities this kilometre limit is a deal breaker.

You can also expect to be charged penalty fees for dings, damages and considerable wear to the vehicleâs interior, exterior or drive performance at the lease end, whether the lease expires or you end the lease early. And, should you really have commitment issues and want to quit your contract before the termâs end date, be prepared to fork over whatever cash amount remains on your lease, which could be upwards of a few thousand dollars. Although seldom discussed, these additional charges are always outlined in the contract, so be sure to read it thoroughly and pay close attention to the details!

Who pays for insurance on a leased vehicle?

When you lease a car in Canada, you are responsible for paying the insurance premiums, just as you would if you were financing or owning a car outright. However, leasing companies typically have specific insurance coverage requirements, which usually include:

Liability Coverage: This covers bodily injury and property damage to others if you are at fault in an accident. Minimum limits are typically higher for leased vehicles. Collision Coverage: This covers damage to your leased vehicle resulting from a collision, regardless of who is at fault. Comprehensive Coverage: This covers damage to your leased vehicle from non-collision events such as theft, vandalism, fire, or natural disasters. Gap Insurance: Some leasing companies may require or recommend gap insurance. Gap insurance covers the difference between the actual cash value of the vehicle and the remaining lease balance if the car is totaled or stolen. Insurance premiums for leased vehicles can be higher compared to those for financed or owned vehicles because of the higher coverage limits required.

Itâs crucial to maintain the required insurance coverage for the duration of the lease term. Failing to do so can result in penalties, additional charges, or even termination of the lease agreement by the leasing company.Â

Can you return a leased car early?

Yes, you can return a leased car early in Canada, but it often comes with additional costs and considerations. Here's what you need to know:

Early Termination Fees Most lease agreements include penalties for early termination. These fees can be substantial and might include:

Negative Equity If the car's current market value is less than the remaining lease obligations, you may have to pay the difference, known as negative equity.

Lease Buyout Some lease companies allow you to buy out the lease early. This involves paying the remaining lease balance plus any early termination fees. You can then sell the car to recoup some costs, but this depends on the carâs market value.

Lease Transfer In some cases, you can transfer the lease to another person through a lease transfer or lease assumption. However, there may be fees associated with this transfer, and the new lessee must be approved by the lease company.

Trade-In Another option is to trade in the leased car when you buy or lease a new vehicle from the same dealership. The dealer might roll the remaining lease balance into the new lease or loan, but this could result in higher monthly payments.

Steps to return a leased car early:

Buying out a car lease in Canada

Buying out a car lease in Canada involves purchasing the leased vehicle either at the end of the lease term or, in some cases, before the lease term ends. Hereâs a detailed guide on how the process works:

1. Review your lease agreement Check your current lease agreement for the buyout terms, including the residual value (the car's estimated value at the end of the lease). This is the amount youâll pay to buy the car.

2. Determine the buyout timing

3. Evaluate the carâs market value Compare the residual value with the carâs current market value. If the residual value is lower or comparable to the market value, buying out the lease could be a good financial decision.

4. Arrange financing If you donât have the cash to buy the vehicle outright, youâll need to arrange financing. You can: Apply for a car loan from a bank or credit union or you can check if the leasing company offers financing options for the buyout.

5. Notify the leasing company Inform the leasing company of your intention to buy out the lease. They will provide you with the necessary paperwork and the final buyout amount, which may include taxes and fees.

6. Complete the paperwork Fill out and submit all required paperwork, which may include: Buyout form provided by the leasing company and loan documents if you are financing the buyout. 7. Make the payment Pay the buyout amount as specified by the leasing company. This can be done through: A lump-sum payment if youâre paying in cash or financing through a loan if youâve arranged one. 8. Transfer ownership Once the payment is processed, the leasing company will transfer the title and ownership of the car to you. Make sure you receive all necessary documents, including: The vehicle title, bill of sale and lien release, if applicable. 9. Register the car Visit your local provincial or territorial licensing office to register the car in your name. Youâll need to provide:

Benefits of buying out a lease

Below we examine the key differences between leasing and financing the same car as these are the two most popular methods of obtaining a new vehicle in Canada.

Lease: When you lease a new car, youâre essentially renting it for a set period (usually 2-3 years). At the end of the lease term, you return the car and can either lease a new vehicle or choose not to lease another car.

Finance: When you finance a car, youâre taking out a loan to purchase it. Once youâve paid off the loan, you own the car outright and can keep it as long as you want.

Lease: Lease payments are typically lower monthly payments than loan payments because you're only paying for the car's depreciation during the lease term, not the full purchase price.

Finance: Monthly loan payments are typically higher than lease payments because youâre paying off the entire purchase price of the car, plus interest.

Lease: Leases often come with mileage limits, and exceeding these limits can result in additional fees.

Finance: There are no mileage restrictions with financing, so you can drive as much as you want without worrying about penalties.

Finance: Youâre responsible for all maintenance costs and repair costs once the car is out of warranty.

Lease: At the end of the lease you do not own the vehicle. In most cases you will have the option to buy out the car at the end of the lease. Your lease agreement will include the buyout terms, including the residual value, which is the car's estimated value at the end of the lease term. This is the amount you would pay to buy the car.

Finance: When you finance a car, you have the option to sell it or trade it in later. You can also benefit from any resale value it may have.

Can I afford a car loan?

If you'd prefer to take ownership of your next car, an auto loan might be more affordable than you think. It takes seconds to see what your monthly payment could look like with our car loan affordability calculator.

There are a few car leasing options in Canada, and depending on your personal needs and interests, one may be better suited than the others.

Can you get a one-year car lease?

A short-term car lease is typically a minimum of two years. One-year leases are available but theyâre rare. If you do find a dealership offering a one-year lease agreement, youâll find that your monthly payment will be very high due to depreciation. However, you might be able to lease a used car and bypass high depreciation costs. Alternatives to one-year vehicle leases include long-term rentals and a lease takeover.

Leasing a car lets you drive a brand new vehicle without the more expensive cost of purchasing one. Of course, car leases are appealing to many; who wouldnât want to drive a high-end car without the big price?! If youâre one of the many interested individuals, youâve already weighed the pros and cons and now you're wondering âhow do you lease a carâ?

Leasing a car lets you drive a brand new vehicle without the more expensive cost of purchasing one. If youâre one of those interested individuals who has already weighed up the pros and cons and is now wondering âhow do you lease a carâ?

If you're intent on leasing a car, these 9 steps will guide you through the process. In an ideal situation where you know exactly what you want, leasing a car can be done pretty quickly. For others, it may take up to a couple of weeks.

Check Your Credit Score

Remember, you normally need an above-average credit score to get approved for a lease. According to Equifax, any score over 660 is considered good. If youâre not there yet and have poor credit or no credit at all, donât worry! You can check your credit score for free, and there are things you can do to improve your credit too!

When leasing a vehicle, your monthly payment might be lower than if you finance, but you also need to consider a potential down payment, insurance, fuel, maintenance, and more. Itâs wise to sit down and crunch some numbers to make sure you know exactly what you can afford without feeling financially squeezed.

Find the Right Car

Firstly, you need to decide what type of vehicle suits your needs! Maybe you need a big family car, or maybe you need a luxury model for business purposes? Obviously, the internet is a powerful research tool. Google Search and YouTube alone can help you narrow down your choices until you find âThe One.â

Find the Right Dealership

Once youâve chosen a car, itâs best to research different vendors and available offers. Understand all your options so you can negotiate and walk away from a deal if you donât like whatâs being offered.

Book a Test Drive

Take the vehicle you are interested in out for a test drive so you can be sure it meets your requirements and is everything you expected it to be.

Consider a Down Payment

Down payments are not entirely necessary for car leases but are helpful in some instances. For one, money down increases the likelihood of getting approved and reduces your monthly payments. If you don't have the savings to make a down payment, don't worry, a 0 down car lease is possible.Â

Review Your Lease Agreement

Once you select a car and get approved for finance, youâll want to examine your lease agreement closely. Take note of your monthly payment, down payment, length of the term, what maintenance youâre responsible for, and other fees. If you need to change anything at the last minute, you can discuss it with your dealer.

Now that you have a leased car, drive off the lot and start making payments! If you donât miss any payments, a lease can help boost your credit score!

Many people donât need to be told to take care of their car, but itâs worth reiterating for a leased car. Any damage incurred or neglect could end up costing you at the end of the lease term.

If you're leaning towards financing a car instead of leasing, it takes two minutes to know if you're eligible for a car loan by getting pre-approved online. With a pre-approval you can shop with confidence knowing exactly what you can afford.

139.135.55.4

Calculator For Novated Lease

ผู้เยี่ยมชม

iqrasaad091@gmail.com